Disseminating knowledge related to productivity and quality: Material flow cost accounting (MFCA)

Post date: Friday, Dec 1, 2023 | 18:40 - View count: 390

On 01st December, within the framework of the Support Program for Students on Productivity and Innovation activities, Directorate for Standards, Metrology and Quality (STAMEQ) organized a virtual training session about Material flow cost accounting (MFCA).

Attending the online training session were Dr. Ha Minh Hiep – Acting General Director of STAMEQ, Mr. Pham Le Cuong – Deputy Chief of STAMEQ Administration Department, and more than 1,300 lecturers, young profesionals, students at 27 universities and colleges from North to South of Vietnam. Namely as, Academy of Journalism and Communication; Thuyloi University; Academy of Finance; Hanoi Industrial Textile Garment University; East Asia University of Technology; Foreign Trade University; Vietnam Russia Vocational Training College No.1; College of Industrial and Constructional; Mientrung Industry and Trade College; Dong A University; University of Economics, Hue University; Ho Chi Minh city University of Technology, Vietnam National University Ho Chi Minh city; Ho Chi Minh City University of Industry and Trade; Foreign Trade University (campus II); Thu Dau Mot University; Tra Vinh University; Viet Nam National University, Ha Noi; Binh Duong University; Vietnam – Singapore Vocational College; Vinh Long University of Technology Education; Nam Dinh University of Technology Education; University of Economics – Technology for Industries; Nha Trang University; University of Khanh Hoa; Ho Chi Minh Communist Youth Union of Yen Bai Province; Nam Dinh Department of Science and Technology and Ho Chi Minh Communist Youth Union of STAMEQ.

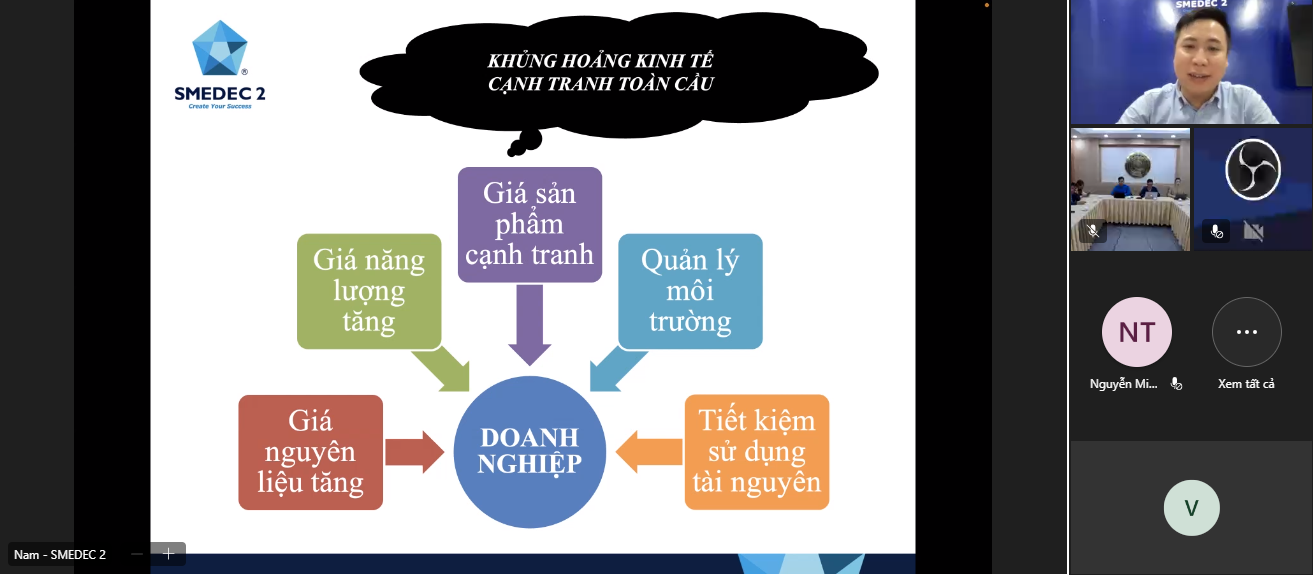

Sharing about topic Material flow cost accounting (MFCA) at the online training session, Mr. Nguyen The Nam – expert consultant at Small and Medium Enterprise Development Support Center 2 (Directorate for Standards, Metrology and Quality) said, MFCA is an environmental management accounting method that allocates costs to material and energy flows through a process, thereby enabling a simultaneous reduction in environmental impacts alongside an improvement in business and economic efficiency.

MFCA first appeared around the late 1980s in Germany and represented the first time that the thermodynamic concept of mass balancing was applied to process flows. It helps manage and optimize the use efficiency of raw materials so this approach has been applying widely in Japanese companies.

As Mr. Nguyen The Nam presented, MFCA method is currently guided by the International Standards Organization (ISO) standard ISO 14051: 2011— Environmental management: material flow cost accounting. The standards define MFCA’s key terms and definitions, its fundamental elements and basic steps for its implementation. According to DIN ISO 14051, “MFCA is a management tool that can assist organizations to better understand the potential environmental and financial consequences of their material and energy use practices, and seek opportunities to achieve both environmental and financial improvements via changes in those practices”.

To apply MFCA successfully, enterprises need to equip general knowledge themselves:

– Input data collection: Enterprises need to have some specific information and details concerning kinds of materials used for product manufacturing as well as raw materials, such as main materials, subsidiary materials, water and energy.

– Output data collection: Output results in process embrace products, non-product factor (waste, material loss). Waste is considered as a factor to reflect the performance of material use.

MFCA brings about both environmental and cost-reduction impacts on the organization. In order to apply MFCA to an organization effectively, the concepts of quantity center, material balance, cost calculation need to be incorporated.

- Quantity center

A quantity center is typically one or multiple unit process(es). The center is the point at which the material balance will be calculated both in physical and monetary units. One quantity center can include either a single process or multiple processes, depending on the amount of the material losses identified at the unit of production. Furthermore, the quantity centers within the MFCA boundary can be based on existing production management information, cost center records, and other existing information.

Once the inputs and outputs have been identified for each quantity center, they can be used to connect the quantity centers within the boundary so that data from the quantity centers can be linked and evaluated across the entire system within the scope. It is important that material balance be ensured to evaluate material efficiency in physical and monetary units.

- Material balance

In MFCA, all material that goes into and leaves the quantity center should be balanced. Thus, to account for all the materials targeted in the MFCA analysis, the material input and output need to be confirmed, while comparing the quantities of material inputs to outputs and changes in the inventory to identify any data gaps. The missing materials or other data gaps can lead organizations to identify missing points which result in areas of improvement.

A material balance requires that the total amount of outputs (i.e., products and material losses) be equal to the total amount of inputs, taking into account any inventory changes within the quantity center. Ideally, all materials within the MFCA boundary should be traced and quantified. However, in reality, materials that have minimal environmental or financial significance can be excluded.

- Cost calculation

During the decision-making process, financial considerations are often included. Through MFCA, the material balance of inputs and outputs is linked to monetary units by assigning and/or allocating costs to all products and material losses. MFCA considers four types of cost, all of which are allocated to both products and material losses:

- Material costs;

- Energy costs;

- System costs; and

- Waste management costs

In order to give students better understandings about this week’s topic, the experts have given many illustrative examples as well as steps of MFCA implementation to give students a direct view more clearly, from which it can be recognized and applied to their future life and work.

The virtual training session kept attendees engaged and received lots of interesting questions from students. All questions have been satisfactorily answered by STAMEQ experts.